Recently, the price of lithium carbonate has once again reached 200,000 yuan per ton, and sodium-ion batteries have begun to move from being a “potential technology” to the stage of mass production. The key to this round of changes not only indicates that after the rapid rebound of lithium prices, sodium batteries will soon witness a significant increase in production, but also means that the most core “low-cost logic” of the entire energy storage industry over the past few years is being rewritten.

Expected reversal, lithium carbonate price returns to 200,000 yuan/ton

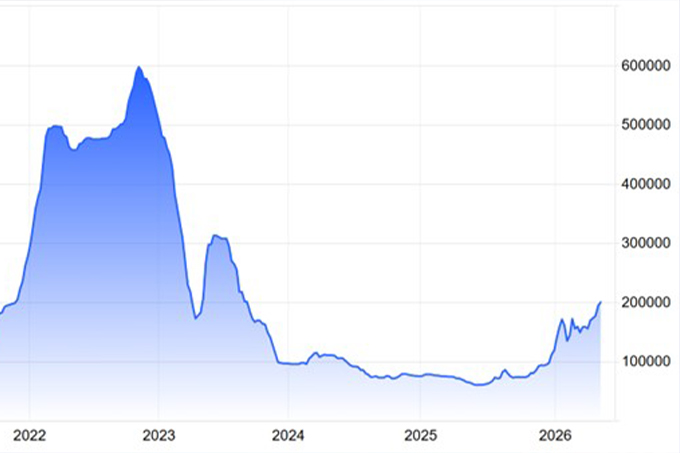

In May 2026, the lithium battery industry is undergoing a typical “reversal of expectations”. Earlier this year, at the beginning of the year, the market’s assessment of lithium carbonate was still rather pessimistic. At that time, the price of lithium carbonate had just rebounded from a historical low of 58,000 yuan/ton in 2025 to around 130,000 yuan/ton. The industry generally believed that after an increase of over 120% previously, the lithium price had approached the peak of the stage.

Figure: Trend of Lithium Carbonate Prices in the Past Five Years

However, contrary to market expectations, the price of lithium carbonate did not stop rising in 2026. On May 11th, the main contract of lithium carbonate on the Guangzhou Futures Exchange broke through the 200,000 yuan/ton mark, with an annual increase of over 67%, and once again reached a new high in the past two years. The price of battery-grade lithium carbonate in the spot market also approached 200,000 yuan/ton. The underlying reason for this round of rise was not simple speculation, but rather a typical “demand explosion + supply shortage” dual driving force.

Over the past few years, battery power has been the core driver of lithium demand growth. However, since 2026, energy storage has truly taken over the baton. The demand for energy storage in AI data centers, overseas large-scale storage, residential storage, domestic independent storage, and storage at the source and grid sides has expanded simultaneously. For the first time, energy storage has truly become one of the core engines driving the growth of lithium demand. Some institutions have even directly raised their forecast for the global growth rate of energy storage demand in 2026 to 60%.

In particular, the rise of AI data center energy storage is becoming the biggest new variable in this round of demand-side. As the global AI computing infrastructure enters a stage of rapid construction, the demand for high-reliability, high-cycle, and high-power energy storage systems in data centers has rapidly increased. Energy storage is no longer just an auxiliary facility for new energy, but has begun to become a part of the AI infrastructure.

Meanwhile, the supply side failed to release its elasticity simultaneously. Affected by factors such as the suspension of some lithium mines in Yichun, Jiangxi Province, the environmental rectification in Qinghai Province, and the restrictions on lithium concentrate exports in Zimbabwe, the global lithium resources remained tight in the short term. When the expansion rate of demand far exceeded the recovery rate of supply, the lithium price entered a strong upward cycle again, completely breaking the previous two-year industry’s fixed belief that “the price of lithium batteries would only continue to decline”.

The era when “battery cells will become increasingly cheaper” may be coming to an end.

Over the past two years, the entire energy storage industry has almost reached a consensus: as technology matures and scale expands, the price of battery cells will continue to decline. Therefore, when calculating the economic viability of numerous energy storage projects, they all assume that the cost of equipment will keep decreasing in the future. Many enterprises even rely on “future price reduction of battery cells” to maintain the return on their projects.

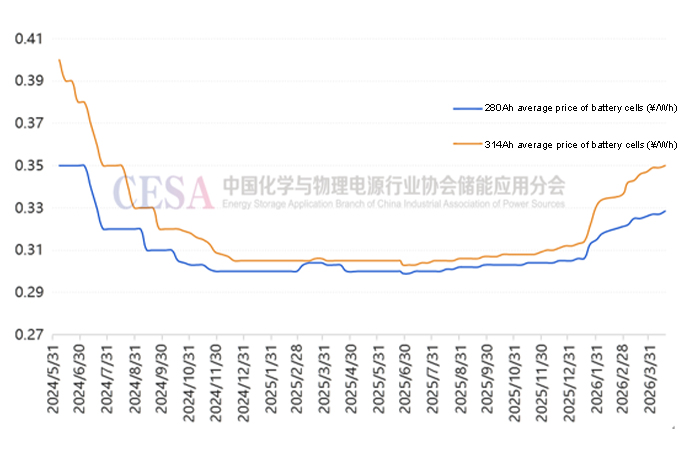

However, after 2026, this logic began to fail. As lithium carbonate prices rose again, the prices of energy storage cells also entered an upward trend. Currently, the prices of first-line brand energy storage cells on the market have once again approached 0.4 yuan per watt-hour, while previously the industry generally believed that prices below 0.3 yuan per watt-hour would become the long-term trend.

Figure: Trend of domestic lithium iron phosphate battery cell prices in the past two years

It’s not just the battery cells that have seen price hikes; the quotations for PCS, system integration, and EPC have also all risen significantly. A large number of projects that previously relied on low-bid contracts are now facing the risk of cost out-of-control, and some projects have even experienced delays, defaults, or renegotiations.

In the past, the core of industry competition was “low-price competition”. Many enterprises believed that they could secure projects by offering extremely low quotations initially, and then continue to lower the price of the battery cells to earn profit margins. However, now the industry has discovered for the first time that battery cells have not continued to decrease in price; instead, they have started to rise. As a result, a large number of energy storage investors have begun to face an extremely realistic problem: the later the project is built, the worse the IRR (Internal Rate of Return) will be.

For the energy storage industry, this actually represents a fundamental restructuring of the underlying logic. In the past, the industry benefited from the “dividend of continuously declining costs”, but in the future, the truly important competitiveness may no longer be just low prices, but rather who can consistently secure supplies, control costs, and ensure the security of the supply chain during price fluctuations.

And this, precisely, opened up the opportunity for the industrialization of sodium-ion batteries.

Sodium batteries have entered the window period for industrialization.

Over the past few years, sodium-ion batteries have been in a state of “long-term optimism but short-term difficulty in implementation”. The core reason is very simple: when the price of lithium is sufficiently low, sodium batteries are difficult to demonstrate a significant economic advantage. Especially after the lithium price dropped to the range of 50,000 yuan/ton in 2025, the market once believed that the window period for sodium batteries had closed because at that time, lithium iron phosphate was already sufficiently cheap, and sodium batteries could hardly form a large-scale substitution.

After 2026, the national level significantly increased its support for sodium-ion batteries. In the 2026 government work report, it was clearly stated that a planning outline for the construction of an energy power country would be formulated, promoting the independent control of key technologies for new energy at the national strategic level. In January 2026, the Ministry of Industry and Information Technology, the National Development and Reform Commission, and eight other departments jointly released the “Action Plan for High-Quality Development of New Energy Storage Manufacturing”, clearly stating the promotion of technological research and development and large-scale application of sodium battery energy storage systems. In the same month, the “Guidelines for the Construction and Application of Industrial

Green Microgrids (2026-2030)” further proposed promoting the application of sodium-ion batteries in industrial microgrid scenarios.

Meanwhile, the industry standard system is also accelerating its improvement. The group standard “Technical Requirements for Sodium-Ion Batteries for Energy Storage” has been released, and national standards such as “Safety Technical Specifications for Sodium-Ion Batteries and Battery Packs for Electrical Energy Storage Systems” have begun to solicit public opinions, indicating that the sodium-ion battery industry is moving from the stage of technological exploration to the stage of standardization development.

Compared with lithium batteries, the greatest advantage of sodium-ion batteries lies in their safety and wide temperature range adaptability. Hu Yongsheng, the chairman of Zhongke Haishan, pointed out that the starting temperature of thermal runaway for sodium-ion batteries can reach above 200℃, and the self-heating rate is significantly lower. They can avoid fire and explosion even under extreme conditions such as puncture, short circuit, and overcharging.

Low-temperature performance is a significant competitive advantage of sodium batteries over lithium batteries. Traditional lithium iron phosphate batteries typically lose 70% to 80% of their capacity at -20℃, while sodium-ion batteries can still maintain over 90% capacity at the same temperature. For instance, the “NaXin” power battery from Ningde Time even retains 90% usable capacity at -40℃ and supports peak 5C fast charging. The new generation product from Zhongke Haishan covers a working temperature range of -40℃ to 60℃, and has a fast charging cycle life of over 8,000 times. This low-temperature advantage means that sodium-ion batteries are naturally suitable for extremely cold scenarios such as in Northeast, Northwest, and high-altitude mountainous areas, and possess differentiated competitiveness in areas such as energy storage, low-speed vehicles, and commercial vehicles.

In terms of cost, according to the data disclosed by Zhongke Haishan, the cost of sodium-ion battery cells has decreased from 0.8 yuan/Wh in 2023 to 0.35-0.40 yuan/Wh in the first quarter of 2026. The cost gap with lithium iron phosphate batteries has narrowed to approximately 0.10 yuan/Wh. The industrial cost curve is rapidly declining.

Therefore, many industry experts believe that in the past, discussions about sodium batteries mostly remained at the “alternative technology” level. However, starting from 2026, sodium batteries have truly entered the commercialization window period.

Sodium batteries will change the pricing logic for lithium prices.

Many people still understand sodium batteries within the framework of “replacing lithium batteries”. However, in reality, the truly significant meaning of sodium batteries is not replacement, but rather reconstruction.

In the era of lithium batteries, the entire industry chain was highly dependent on lithium resources. Whoever controlled the lithium mines would have the power to set the prices. However, with the emergence of sodium batteries, a new industrial logic has begun to take shape, that is, the future energy storage system is likely to be an era where both “lithium” and “sodium” routes coexist.

Lithium batteries are suitable for high energy density and high-performance scenarios; sodium batteries are suitable for low-cost, long-duration energy storage, and wide temperature range scenarios. Once this system is established, the fluctuation logic of lithium prices themselves will also change. Because sodium batteries will naturally form a “price constraint mechanism”: when lithium prices are too high, some energy storage demands will shift to sodium batteries; and when lithium prices fall again, lithium batteries will regain their economic advantages.

This means that in the future, the upper limit of lithium prices will be redefined by sodium batteries. That’s why leading battery companies are now simultaneously developing lithium batteries and sodium batteries. What they are competing for is not a specific technological route, but rather the control of the discourse in the future energy storage system.

The challenge of sodium batteries is not the technology, but the pace of industrialization.

Of course, sodium batteries are not without risks. The real issue, in fact, is not the sodium battery technology itself, but the pace of industrialization.

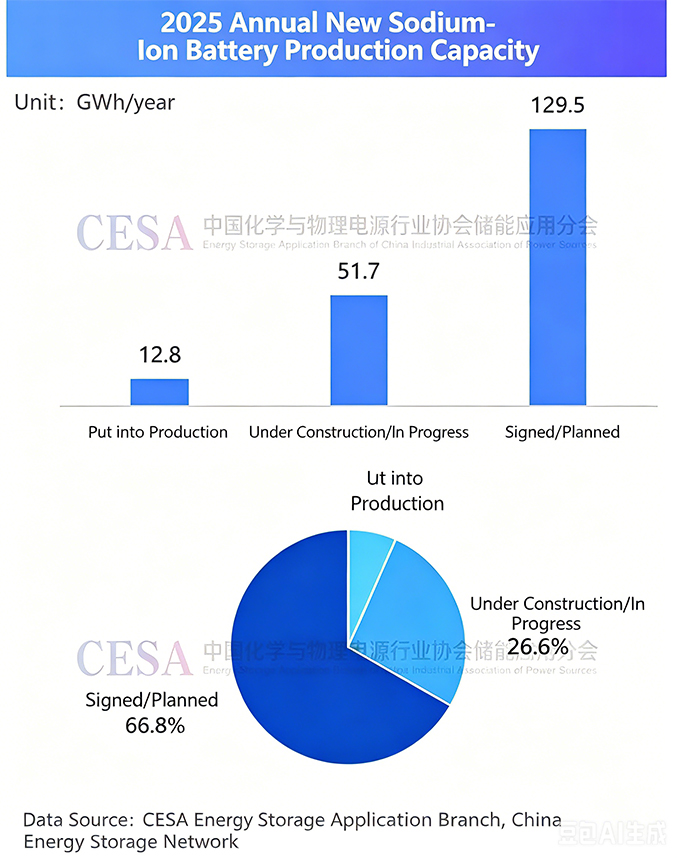

The first challenge is production capacity. The 60GWh order is undoubtedly wonderful, but behind it means that the entire industry needs to rapidly expand production. However, sodium batteries are still in the early stage of large-scale production. According to the industry database of the CESA Energy Storage Application Association, by the end of 2025, the annual production capacity of sodium-ion batteries in China will reach 29GWh, with 173GWh under construction and 300GWh planned. The total planned investment will exceed 190 billion yuan. In 2025, a total of 50 sodium-ion battery production and manufacturing projects were newly added in China, with a planned annual production capacity of 194GWh. Among them, 41 projects disclosed the investment amount, totaling 79.6 billion yuan, with an annual output value of 63.2 billion yuan after commissioning, and an additional production capacity of 12.8GWh and an additional started or under-construction capacity of 51.7GWh.

The second challenge is hard carbon. The core material of the sodium anode is still hard carbon, and the current production capacity of high-end hard carbon is still limited. The yield, consistency and cost all need to be further optimized.

The third challenge is global certification. Currently, the largest growth market in the global energy storage sector still comes from overseas. However, the certification process for new energy storage technologies in the European and American markets is extremely lengthy. The domestic market can advance rapidly, but the overseas market may not be able to achieve the same level of expansion simultaneously.

Therefore, in the next two years, the industry really needs to focus on observing only three indicators: first, whether the sodium battery energy storage projects can continue to expand; second, whether the cost of sodium batteries can continue to approach or even be lower than that of lithium iron phosphate batteries; third, whether the industrial chain support can keep up with the pace of large-scale production.

Only when these issues are gradually resolved can sodium-ion batteries truly enter the global mainstream energy storage system as an “alternative energy storage technology”.

Conclusion: The energy storage industry will move towards “coexistence of multiple technologies”

Over the past few years, the biggest advantage in the energy storage industry has come from “low cost”. However, in the future, the competitive logic of the industry has changed. What truly determines a company’s competitiveness may no longer be just price, but rather technical route capabilities, multi-system switching capabilities, supply chain control capabilities, and full life cycle LCOS capabilities.

Some industry insiders believe that in the future, the energy storage industry will gradually evolve into a system featuring “multiple technologies coexisting”. Lithium batteries will not disappear, and sodium batteries will not merely serve as a supplement. The two will form long-term synergy in different scenarios. The truly dangerous aspect is not the change in technological routes, but the continued adherence to a single-path thinking. Because the most crucial change in the entire energy storage industry has shifted from the era of a single technology path to a multi-faceted system era.